Copperstone PFS Released

What Just Happened, and What's Next: A Post-Release Read

Minera Alamos Inc. (TSX-V: MAI | OTCQX: MAIFF)

May 30, 2026

Spot Gold: US$4,500/oz

Minera Alamos released the Copperstone pre-feasibility study on May 27 after market closed. The Board approved a formal construction decision.

What the PFS settles is whether Copperstone gets built. The answer is yes, and on terms that are favorable. What it does not settle is how big the asset ultimately becomes. That question lives in the open-pit work coming behind it, in the resources still to be drilled out, and in the corporate sequence that turns a development project into a multi-asset producer over the next eighteen months. This note walks through what was disclosed, what it confirms about the investment case, and what’s left to play out over the rest of 2026 and into 2027.

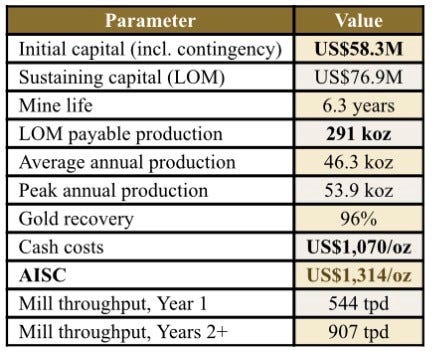

Initial capex of US$58 million. Payback of 1.2 years at the base case gold price, and 0.8 years at spot. Fully funded from cash, the revolving credit facility, and Pan free cash flow, no equity raise required. After-tax NPV5% of US$374M at the base case US$3,500 gold, and US$537M at US$4,500 spot. Capital intensity of 6.4x base / 9.2x spot. Construction decision approved.

The Headline Economics

The PFS shows a high-return, low-capital underground gold project. All figures below are taken directly from the May 27 disclosure.

The cost performance came in much better than I anticipated. Cash costs at US$1,070/oz and AISC at US$1,314/oz is very encouraging given the inflationary cost environment seen in the Gold mining sector. The operating team appears to have found efficiencies that don’t show up in the raw inflation math as well as utilizing refurbished equipment. Looking forward to reading the technical report when it comes out in 45 days.

NPV Sensitivity (from PFS Table 2)

What the PFS Confirmed About the Investment Case

Four elements anchor the investment story at Copperstone. The PFS confirmed all four, some more strongly than I expected going in.

I. Capital Intensity: Confirmed and now Quantified

US$58M of initial capital against a project that pays itself back in 1.2 years at the base case and 0.8 years at spot. NPV/Capex of 6.4x base and 9.2x spot.

Those multiples sit well above the peer median for North American underground gold development. The reason is Copperstone’s brownfield infrastructure, which includes approximately 4 km of pre-existing underground development, a fully permitted tailings facility, surface buildings, an installed grid power connection, refurbished equipment, and a partially complete process plant. A greenfield equivalent would cost materially more.

The PFS mine plan also took the opportunity to expand the process plant from the PEA’s 600 tpd to 1,000 tpd from Year 2 onward, with a planned three-month ore stockpile to de-bottleneck commissioning. This is a deliberate scope upgrade, and it’s what drives the production profile up from 40k oz/yr to 46k oz/yr average.

II. Resource Conversion Opportunity

The PFS published a maiden Proven & Probable reserve of 303 koz at 4.87 g/t. This is the inventory feeding the published mine plan. This reserve is drawn from a substantially larger Measured & Indicated resource of 630 koz at 4.83 g/t (Resources are reported inclusive of Reserves) a 110% increase versus the previous resource estimate. Higher Gold prices and a lower cutoff grade was the material driving factor here.

The residual, 328 koz of M&I and 52 koz of Inferred, sits outside the published mine plan, per the company’s investor presentation. That is a meaningful inventory of known, drilled material that has not been pulled into the reserve through PFS-level modifying factors. None of it is in the published NPV. Every successful conversion adds incremental ounces. According to the latest Stifel analyst report entitled Copperstone PFS largely in-line with our estimates, it states that “each additional year of operation is estimated to increase the NAV for Copperstone by 9% and adds approximately US$0.32 per share.” The company has indicated infill drilling is planned to occur largely from underground starting in 2027, with a resource and reserve update targeted for 2028. The down-plunge extension potential will be further evaluated from underground drill stations once mining is underway, which is the most cost-effective way to add reserves at a producing mine.

III. The Open Pit: Additional Opportunity

This is the driver that does the most work in the post-PFS story, and the investor presentation released alongside the PFS provides more specificity than the press release alone.

Copperstone historically operated as an open-pit mine and produced approximately 514,000 ounces of gold from surface ore between 1987 and 1993. The company has identified two initial open-pit zones of interest, West OP and East OP, and a 2026 RC drill program is planned to test these zones commencing in Q3 2026 per the company’s timeline.

Historical drill intercepts in these zones include:

70m grading 4.3 g/t Au

35m grading 3.1 g/t Au

49m grading 1.2 g/t Au

Additionally, per the company’s investor presentation: “Some resources were excluded from mine plan and not converted to reserves because they are above the existing pit-bottom elevation (~152m from surface), and may be more economical to mine via open pit methods in the future.”

Near-surface ounces have been held back from the underground reserve because they likely belong in the future open-pit study. The PFS is, by design, a snapshot in time. However, there is another element to the project: the maiden open-pit resource scheduled for later in 2026, with open-pit development studies and permitting running thereafter.

The company has stated that an open-pit operation would require additional permitting but could potentially be developed as a separate heap leach facility on site, concurrent with underground production. This implies a future two-front operation, not a substitution to the underground. Underground keeps producing 46+ koz/yr; the open pit eventually adds incremental ounces on top of that, all while extending the mine life of the overall operation.

Higher gold prices have materially changed what an economic pit shell looks like. At US$1,800 gold the shell is smaller. At US$4,500 Gold it expands considerably as more peripheral and shallow material becomes economic. Nothing about open-pit potential is in the published PFS or in the NPV figures above, which is another opportunity value creation driver.

IV. What Minera Paid: The Acquisition Math

Minera Alamos acquired Copperstone through the Sabre Gold Mines transaction announced October 28, 2024, and closed February 6, 2025. Under the deal, Minera issued approximately 76.5 million shares (pre-consolidation) to acquire all of Sabre’s outstanding stock. With Minera shares trading in the C$.30 to C$.40 range over the announcement-to-closing window, the implied total equity consideration was approximately C$23M to C$30M, or roughly US$17M to US$21M at then-prevailing exchange rates.

Gold was trading near US$2,700 per ounce at the time. Minera paid roughly US$21M of equity to acquire an asset that just printed a US$374M base-case NPV, and a US$537M NPV at spot. With the earlier acquisition of the Pan Mine providing the cash flow base to fund Copperstone’s construction without dilution, the acquisition math comes full circle. Whatever you think about the asset on its own terms, the setup for a re-rate is an optimal one in junior gold development.

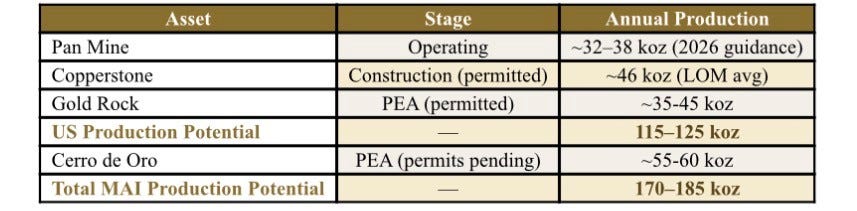

The Corporate Picture: Forward Guidance Path to 170 to 185 koz/yr

The Pan mine in Nevada is currently guiding to 32–38 koz of gold production in 2026. Copperstone, once ramped, will add approximately 46 koz/yr average and 54 koz at peak. Per the company’s May 2026 investor presentation, the broader portfolio path looks like this:

Re-rates in junior gold tend to track production milestones from developer to producer. Pan is currently in production. Copperstone is the most immediate production milestone, with first gold targeted for mid-2027 and a more-than-doubling of consolidated corporate output once ramped. Gold Rock then follows in H2 2027 and Cerro de Oro in H2 2028 (subject to permitting).

The market context for that re-rate matters. Per management’s May 2026 deck, MAI currently trades at approximately 0.35x consensus P/NAV versus a peer average of 0.47x. The company also screens at the top of its peer group for consensus 2026–2029 production CAGR showing 68% growth, the highest in the comparable set. That combination, which includes bottom-of-peer valuation, top-of-peer production growth, fully funded growth pipeline, is the structural setup for a re-rate over the next 12-24 months provided they execute accordingly.

Funding: Fully Funded, No Material Dilution

Minera Alamos entered PFS season with approximately US$46M of unrestricted cash and a recently closed US$75M revolving credit facility with Scotiabank and National Bank (with US$30M of remaining capacity at signing, per the company’s deck), and the Pan mine continuing to generate monthly free cash flow at current gold prices. Against a US$58.3M initial capital requirement spread over an approximately twelve-month construction window, the project is fully funded internally without an equity raise. The increase in capex from the PEA’s US$36M to the PFS’s US$58M reflects the expanded process plant (600 tpd to 1,000 tpd) and the planned ore stockpile, which are upgrades, not cost overruns. There was an inflationary aspect to the higher ticket capex but there were certainly plenty of offsets.

They already have an embedded financing mechanism with the warrants at C$7.05 that mature in 2028. If the company continues to execute and stage its assets in sequential order, free cash flow should rise significantly and eliminate any meaningful dilution aspect from the equation. That sets up substantial earnings per share growth flowing through to shareholders. If that happens, the warrants will then be exercised, and at that point the company will be flush with an additional US$200M in cash, providing a sizable financing base for subsequent project development or other value creation opportunities. Based on the factors at play today, an equity raise isn’t necessary.

Key Risks

The drivers above describe the upside case. The risks below describe what could go wrong. Readers should weigh them honestly and discount accordingly:

Execution risk

Copperstone capex escalation

Copperstone open-pit permitting

Cerro de Oro permitting

Gold price risk

Project sequencing risk

Dilution risk

Thesis predicated on successful buildouts of each project

What’s Next: The Forward Calendar

The PFS was the most consequential disclosure on Minera Alamos’s calendar this year (setting aside a Cerro De Oro permit), but there is plenty of value creation catalysts moving forward that should keep the management team busy:

Now underway: Copperstone construction activities

June 25, 2026 AGM: Shareholder vote on corporate rebrand from Minera Alamos Inc. to Mining Americas Inc.

Late Q2 2026: TSX main-board uplisting from the TSX Venture exchange (on company timeline)

Late Q2 2026: Copperstone drill program commences, targeting West and East open-pit zones

Q3 2026: Copperstone maiden open-pit resource estimate

Q3 2026: Cerro de Oro federal permit (anticipated but speculative)

Q3 2026: GDXJ potential inclusion (speculative)

Q4 2026: Gold Rock technical report

Q1 2027: Cerro de Oro updated technical report

2026–2027: Copperstone open-pit development studies and permitting

Mid-2027: First gold pour at Copperstone

Mid-2027: US senior exchange listing (NYSE or NASDAQ, per company timeline)

2028: Updated Copperstone reserves and resources (following 2027 underground infill drilling)

The PFS settled the question of whether Copperstone gets built. It did not settle the question of how big and how valuable the asset ultimately gets.

Whether Minera Alamos is reasonably priced today relative to the risk is a question every reader has to answer for themselves. What the PFS settles is that the project moves forward. What management still has to demonstrate is execution. What the market still has to decide is whether to pay for it.

Disclosures

This note is the personal research and opinion of the author. It is not investment advice and should not be relied upon as such. The author is not a registered investment advisor and is not compensated by Minera Alamos Inc. or any party referenced. Past performance and historical analysis are not indicative of future results, and nothing in this note constitutes an offer to sell or a solicitation of an offer to buy any security.

The author owns shares of Minera Alamos Inc. and may buy or sell shares at any time without notice. Readers should assume the author’s views are influenced by this position.

All figures cited in this note are taken from the Company’s May 27, 2026 news release announcing the Copperstone Pre-Feasibility Study results and the Company’s May 2026 investor presentation. The associated NI 43-101 technical report is expected to be filed on SEDAR+ and the Company’s website within 45 days of the release. Forward-looking statements are subject to substantial risk; mineral resources are not mineral reserves and do not have demonstrated economic viability. Statements about future events, projected production, hypothetical gold-price scenarios, and catalyst timing reference Company disclosure and are subject to risks identified in the Company’s continuous disclosure documents on SEDAR+. Readers should conduct their own due diligence and consult qualified professionals before making investment decisions.